Photo: wikipedia.org

Mick Mulvaney, the interim head of the Consumer Financial Protection Bureau (CFPB) told a group of banking executives yesterday that it was their job to persuade Congressman on policy decisions and when he was a Congressman he only talked to lobbyists who contributed to his campaign. At least he is honest about how corrupt his motivations are; he operates on ‘pay to play’ basis. He does say that constituents are top on his list when they sit out in front of his office. But, who does he listen to and represent? His first priority should be consumer protection.

Since coming to the CFPB he has called off investigations into payday lenders, limited or cancelled investigations of banks and other lenders, reduced public access to information about financial services practices and now wants to end its independent funding from the Federal Reserve (to keep Congress from meddling in it investigations).

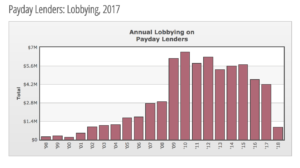

Based on his actions, not words we know now he works for the payday lenders not consumers. He received almost $63,000 for his campaign in 2017 from the Pay Day Lender lobbying association. The Pay Day Lender group spent $4.175 million in 2014 on lobbying activity to keep its predatory practices going with limited restraints. Fourteen states have outlawed pay day lending completely while 36 states and the District of Columbia allow payday lending with some limiting the percentages charged.

Source: opensecrets.org

Payday lending markets to low income borrowers who can’t otherwise get access to a small loan, many do not have bank accounts and some are immigrants. Most do not have good credit or limited credit records so they are willing to pay 400 % or 1209 % with fees for some loans. This practice is usury at its worst. The CFPB found that 4 of 5 loans were rolling debt into larger and larger loans forcing borrowers into a position of not being able to pay back the loan. The agency fined ACE Cash Express $10 million for bullying practices forcing consumers into cycles of debt. Major banks participate in this market too as Wells Fargo offers a ‘Direct Deposit Advance’ service for 120 %.

Next steps:

- Phase Out the Industry – just because these companies can do it does not mean we should make loan sharking legal. There are other answers, already 14 states figured this moral issue out.

- Micro Loan Model – the micro loans offered in emerging countries like India have been quite successful, charging fair interest fees using the Internet and cell phones to keep costs low, and credit counselors to teach borrowers good credit management practices. We need to help low income people learn about responsible credit management not make them prey for companies.

- Limit Lobbying Funding – Pay Day Lenders and other companies should be limited in the campaign funds they give to candidates to what citizens are limited to $2400. After all, based on the Citizens United decision if corporations are people then we should treat them like citizens not special entities.

- Directors and Government Leaders Recusal – Any government official with a financial interest from the last 5 years needs to recuse himself or herself from any decision making on the matter affecting the industry.

- Ethics Violation for Corruptions – any pay for play scheme even without a direct quid pro quo time frame is unethical, immoral and unjust. Any official changing government policy for an entity that they received funding from in the last 5 year should be found in violation of government ethics law, fined, released from his/her position and for severe offenses jailed.

- End Lobbyist Revolving Door – 75 % of lobbyists for Pay Day Lenders end up in government jobs, this practice needs to stop, with no lobbyist working in government for 10 years. We noted how harmful this practice was in our blog on December 14th archive on the new FCC Chairman being a former cable industry lobbyist.