Image: debt.org

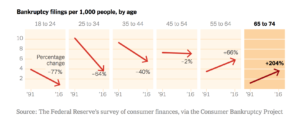

Researchers tracking the financial blight of seniors report that seniors over age 65 are 3 times more likely to file for bankruptcy. Seniors are caught by reduced pensions, co pays on their children’s student loans, spiraling medical costs and lost wealth from the Great Recession.

Sources: Consumer Bankruptcy Project, The New York Times – 8/3/18

The post – Baby Boomer generation is feeling squeezed too as their bankruptcy filings are up over 66 % for the 55 to 64 year old group. Many Baby Boomers just beginning their retirement or in the their last years of savings were hit hard by the Great Recession, wiping out 401k investments in stocks and losing home equity wealth too. In all households lost $14 trillion in wealth, most of the income and asset recovery of the past 10 years has gone to the top 10 % in income.

The Consumer Bankruptcy Project is an ongoing effort led by Professor Thorne, University of Idaho; Professor Lawless; Pamela Foohey, a law professor at Indiana University; and Katherine Porter, a law professor at the University of California, Irvine. Their universities fund the project as they review court documents and send out questionnaires to retirees.

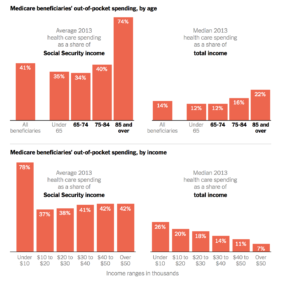

Social Security has not been able to fill the gap. Nor was Social Security designed to be the sole source of income for seniors – it was setup to supplement pensions and savings. Over the past 30 years corporations have shifted from defined benefit (pension direct payment) plans to defined contribution plans like 401k where the worker makes the majority for the contributions and the employer is off the hook to make direct fixed payments. Yet, today for 33 % of retirees receiving Social Security it provides 90 % of their income. Medicare and drug costs cut into their Social Security checks:

Sources: The Kaiser Family Foundation, The New York Times – 8/3/18

Health care spending for the average retiree is increasing every year beyond Social Security income and drugs become more expensive, some with standard prices of $70 per dose gauged up in price to $1700 per dose.

Adding insult to injury firms like AT & T are contracting with collection agencies to claw back overpayments to pensioners. The firms make up the calculation tables and send out the checks now they blame the pensioner, who has already spent the money. It is important if the retiree receives a statement of planned disbursements to send back incorrect checks, however in most cases the checks were sent over some years until the error was found and the retiree had no idea that there was an overpayment.

Next Steps:

The perfect financial storm for retirees comes down to the basic fact that corporations shifted their responsibility for pensions onto workers helping the financial services industry sell more financial products to an naïve and financial challenged workers. Professional financial managers were replaced by amateur workers doing their best to invest their 401k plans and save for the future. For the bottom 80 % income the last 30 years their wages have been stagnant with increasing educational costs for their children and increasing medical costs for themselves. The federal government has been of little help, not indexing Social Security payments to the actual costs seniors incur for increasing medical and health services costs.

- Pension Claw backs – this makes no moral sense, many retirees have spent 20 or 30 years of their lives for the business, the business made the mistake they need to take care of it. In AT & T’s case they spend billions on stock buy backs to make their executives and shareholders rich, they could take a fraction those funds and take care of their seniors and fund their pension liabilities appropriately.

- Retirement Income – in previous posts we have recommended that instead of an incredible mess of 401k accounts, financial houses and amateur investment management by workers, a guaranteed retirement program be implemented starting at the time a person begins work and receives his Social Security card. Worker savings toward retirement would be transferred into this one account for a lifetime, with Social Security contributions by the federal government, and savings by the worker. A portion would be guaranteed by the federal government and professionally managed as a defined benefit plan. Workers could opt for professional management of all their funds as well.

- Medical Costs – as we have recommended health insurance should be run by one entity the present Medicare operation for all Americans from the time of birth. Medicare already has a formulary for drugs, and should be authorized to negotiate drug costs for all patients. Standard compensation for procedures and quality of care implemented for Obamacare should be extended. Drug companies will no longer be able to buy back their stock, but instead will be required to spend those funds to bring drug costs down, or reduce costs in other ways. Direct prescription drug advertising should be outlawed to save the over $1 billion spent a year in wasted advertising and spend the funds on price reductions.