The View:

Researchers estimate that 4.3 million seniors are living in poverty or near poverty today. The number of seniors in poverty is expected to soar by 146 % between 2013 and 2022. Millions of Americans between age 50 and 65 lost their home equity and savings in the Great Recession. They were not made whole then while bailouts were provided to banks and investment houses. The loss of retirement savings and limited social security income results in dire financial straits for many seniors. Retirees are squeezed between student debt (taken on for children and grandchildren), auto loans, medical costs other debt and their fixed income. The patchwork of 401k, IRAs, Roth IRAs, and SEP programs is total inadequate to provide a foundation for a secure financial future for retirement. The Solution is to setup a Retirement Savings Account that includes Social Security when first entering the workforce, with professional management of retirement funds in secure investments guaranteeing adequate income to be above the federal poverty level at age 65. Two-thirds of the funds and Social Security would go toward the poverty threshold providing retirees with an option of investing the other 34 % themselves.

The Story:

“The idea of our financial future being secure was an illusion!” Bob declared, an Amazon Campforce worker about the loss of his home and savings in the 2008 Great Recession. Bob owned a home with good equity and held hundreds of thousands in retirement accounts – in one year it was all gone. The sad reality is that for most seniors today, their financial future being secure is still an illusion.

Over 10 million people many in their 50s and 60s lost their homes, and home equity totaling $3.3 trillion in the Great Recession of 2008 – 2009. The National Association of Realtors estimates that only 33% of those who lost homes were able to come back into the housing market due to poor credit, lack of financing or the fear of another crash. Retirees lost over $1.4 trillion in the last two quarters of 2008 alone or 25 % of their investments. Professor Teresa Ghilarducci of the New School for Social Research predicts that of the 18 million Americans aged between 55 and 64 years old in 2012 by retirement age 4.3 million will live in poverty or near poverty. She estimates that between 2013 and 2022 the number of people in this group will soar by 146 %.

Yet, banks and investment houses that traded derivatives based on mortgages in 2008 that lost billions of dollars were made whole in the federal TARP bailout program. At the time of bank bailouts many people were holding underwater mortgages and were not made whole by write downs on the principal loans with their banks. On group is illustrative of their plight, senior ‘nomads’ houseless roving in RVs from job to job wherever they can find work. Some lost professional jobs during the recession and were not hired back due to lack of new skills or jobs being downsized.

In her book, Nomadland, author Jessica Bruder offers a definitive narrative of the predicament of work campers and their nomadic life. Few of these people chose this life – they are the consequential damage of the financial crisis who have been left out of the growing economy in the past eight years where 90 % of income growth accrued to the top 1 %. Feeling hopeless to change their circumstance, many see no way out but to move from job to job. Some are more hopeful that if they work hard enough they can buy a home again – however in an economy that drives wealth to the top this is a challenging dream. Seniors in urban areas who are homeless, living in shelters or living in crowded multi-family apartments are in a similar financial condition – they just don’t live a nomad life.

Corporations see an opportunity to gain access to an inexpensive, mobile labor by setting up work camp programs like Amazon’s Camperforce. The company needs a large seasonal workforce to achieve 4th quarter sales goals totaling 33% of its yearly revenue. Amazon offers Camperforce members paid RV campsites near locations like their warehouses, where during the holidays they pull items from shelves and pack shipping boxes. Bonuses of $125 are offered for referrals. This is part time work paying $11.75 @hr, plus overtime, $1.00 @hr completion bonus with no 401k, health care, or security of a full time job. Below is a company website promotion focused on warehouse work in Kentucky and Tennessee that looks like a summer camp:

Source: Amazon – 11/30/17

Yet, Bruder discovered in interviews with Camperforce workers the job experience was far from a summer camp. They work in tough conditions lifting heavy packages, walking miles each day on the warehouse floor with limited breaks. Besides warehouse work, nomad workers seek jobs in agriculture; harvesting sugar beets, flipping burgers at spring training baseball games or other seasonal work. They are living on less than $1000 per month, with some locations having no hot showers or hygiene conveniences. Bruder found many women working long past retirement as in the past had left the workforce causing income gaps, had lower pay than men and little leftover for retirement savings.

In the future the number of seasonal jobs will decline as Amazon has installed over 40,000 warehouse robots in 2016 to do picking and packing with plans to install thousands more in the next 5 years.

Amazon reported in 2014 they had over 2,000 Camperforce members, since then it has grown fast to an estimated at 4,000 the result of hard driving company recruitment programs.

In agriculture there were 3 million migrant workers in the US in 2009, with 20% being seniors or about 600,000 both foreign born and domestic. Domestic workers make up 28 % of the migrant force so in terms of those affected by domestic retirement programs it is estimated to be 168,000, now likely to be much larger group.

These mobile seniors are just the tip of a huge population under stress from the losses of the Great Recession

How many seniors are under financial stress?

In our economy there are still 1.5 million more people working part – time for economic reasons than before the Great Recession, the majority are older workers:

Sources: Federal Reserve Bank – St. Louis, The Wall Street Journal, The Daily Shot – 8/14/17

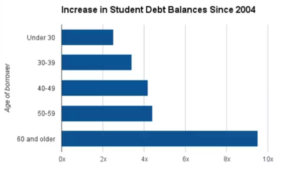

Seniors are taking on more debt for children and grandchildren. Last August, the Federal Reserve reports Parent Plus loans soared to 2 million borrowers in 2015 compared to 1 million in 2003 between ages 50 and 64. There were another 200,000 borrowers over age 64 for similar loans in 2015. The Federal Reserve Bank of New York estimates that Americans over age 60 had a 9 times increase in student debt between 2004 and 2014 to $58 billion.

Source: Federal Reserve Bank – New York – 6/30/15

The Consumer Financial Protection Bureau estimates that 40 % of Americans over age 60 have student debt loads so severe they skipped necessary healthcare. Health care costs continue to grow at a 6.5 % rate according to Price Waterhouse Coopers for 2017, 6 times the rate of inflation at 1.4 %. For older Americans on fixed incomes medical costs are a major component of their expenses with soaring medical costs creating a stressful squeeze on their fixed income budgets.

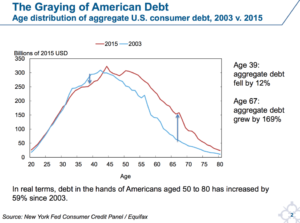

The financial reality for seniors aged 67 is growing worse as their total debt grew by 169 % between 2003 and 2015, they did not receive the uplift in incomes from the growing economy that the top 1% enjoyed.

Sources: New York Federal Reserve Credit Panel, Equifax – 2/12/16

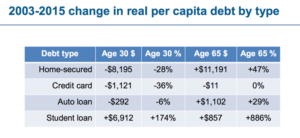

Only 25 % of the increase in senior debt is due to an aging Baby Boomer population. Below is a debt load per capita versus 30 year olds:

Sources: New York Federal Reserve Credit Panel, Equifax, Census Bureau – 2/12/16

The Federal Reserve reported last August that seniors are taking on even more debt. Americans aged 60 and older held 22.5% of total household debt in the fourth quarter of 2016, almost double the debt load of 12.6% in 2003.

The high debt load for those nearing retirement age results from limited participation in savings for retirement. Only 33 % of Americans today are participating in employer 401K plans and on average Americans have only $5,000 saved for retirement, according to the Federal Reserve

The Solution:

Our politicians have designed a failure prone retirement system allowing corporations off the hook providing full defined benefit pension programs with professional management. Instead, 401k employee and employer match defined contribution programs were created where the individual is responsible for investing retirement funds safely. The present retirement program is a patchwork of 401ks, IRAs, Roth IRAs and SEP programs for small business. This mishmash of plans was engineered by the financial services industry to meet their sales and profit goals, yet is missing the continuity, security and financial safeguards that retirement programs demand. The loss of trillions of dollars in the Great Recession clearly demonstrate the failure of the present retirement system which has left millions in poverty or near poverty in their golden years.

Today, Social Security only provides a $12,000 a year benefit to the average retiree. Yet, Social Security provides 80 % of the benefits that 40 % all retired people depend on. A Retirement Savings Account would have as a core principle that the combination of Social Security and worker’s savings provide at least a guaranteed income at the poverty level at age 65.

Beginning with first day of a worker’s first job when they receive a Social Security number they would open a Retirement Savings Account. The worker contributes to the account no matter which employer they are working for the rest of their life until retirement. The Retirement Savings account could be administered by contract to the federal government by a financial services corporation, with the core savings invested by a professional in core income producing and safe investments – Treasuries and federally backed agency issues. Up to 66 % of their retirement funding would be in secured investments with employer matching funds being deposited into the account. If some Americans elect, they can have the remaining 34 % invested in secure defined benefit investments with a guaranteed rate of return at retirement age. Other workers may elect to invest 34 % of their funds in other financial instruments – yet 66 % of their retirement investments would be secured with Social Security making up the majority of the core guaranteed funds.

Funds deposited by workers into their Retirement Savings Account would be tax deferred up to $40,000 per year until age 65 similar to a traditional 401k today. Most workers will see a lower tax rate at retirement as this provision allows for lowering the cost of saving for retirement during high salary tax years. Corporations contributing to a workers’ Retirement Savings Account would be allowed up to a 50 % corporate tax deduction on the matching dollar amount to incent companies to contribute.

There would be no cap on total funds added to the Retirement Account by a worker. Workers would be allowed to obtain a medical or education loan with their retirement account as collateral but only up to 10 % of the value, which if defaulted and not paid back, would be paid back on a pro-rated basis by a Social Security deduction beginning at age 65.

This Retirement Savings Account proposal meets 12 core principle requirements by the Retirement USA, a Washington D.C retirement advocacy group including: universal coverage, secure retirement, adequate income, shared responsibility, required contributions, pooled assets, payouts at retirement, lifetime payouts, portable benefits, voluntary savings, efficient and transparent administration and effective oversight.

Note: References for this post can be found in the Research tab under Retirement.