Image: thinkinnovation

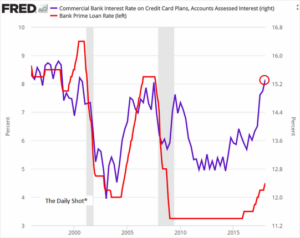

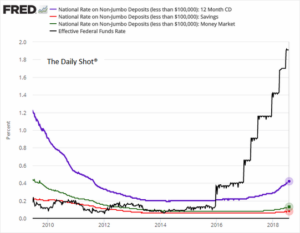

The biggest banks are enjoying high profit margins at the expense of consumers. Today, the rates on savings accounts are the lowest as a percentage of the Federal Funds rate and credit card rates are the highest in proportion to the respective Federal Funds rate. The Federal Funds rate is the rate the Federal Reserve charges banks to borrow money.

Sources: Federal Reserve St. Louis, The Wall Street Journal, The Daily Shot – 8/1/18

Sources: Federal Reserve St. Louis, The Wall Street Journal, The Daily Shot – 7/31/18

The divergence on both charts shows how the consumer is squeezed on both sides of the financial ledger – receiving less for their savings than they should historically and getting charged much more on credit cards than is fair.

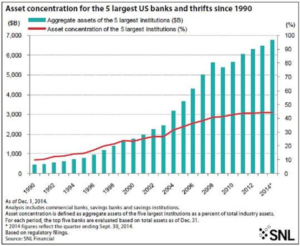

Today, the top five banks control 50 % of all banking system assets in our $15.3 trillion dollar system. In 1990 the five largest banks held just 10 % of all bank assets. The assets that Wells Fargo holds by itself equal all the assets of the top five banks in 1990. As a result of the consolidation during the Great Recession our banking system is highly concentrated in just a few banks.

Next Steps:

The lack of competition is clearly hurting consumers in both financial directions, paying higher interest rates than are fair and not receiving the interest income they should. The key point is that present regulators are not doing their job requiring banks to pay higher interest and keep credit card interest charges in check. Next, from our post on bank concentration we recommended a break-up of the big five banks:

“Experts like Neil Kashkari who led the Bush Administration’s $700 billion bank bailout effort the Troubled Asset Relief Program, thinks these mega banks should be broken up. Now Kashkari is the Federal Reserve Governor for Minneapolis and has called for reducing the size of the big banks and distributing their power and control to provide a better shock absorber in the event of another banking crisis. He even calls for a 25 % capital reserve requirement many times the present capital reserve requirements the Federal Reserve has maintained in its stress test program. We have seen with the failure of Wells to protect its customers from 3.5 million fake checking accounts created by its sales staff how poorly bank management performs. Now, the bank is being investigated for improper referrals and transferring of funds in the wealth management division.

Enough is enough, our present financial system is too concentrated to effectively manage; distributing wealth, power and control back into regions is one way to ensure reasonable oversight and management can prevail. In addition, we support calls for a modern day Glass-Steagall Act to separate investment banking (were sub–prime derivatives of the Great Recession were created) and commercial banking for retail customers. We need to protect our citizens financial assets from the financial engineering and schemes of Wall Street. It is not a coincidence that today 90 % of all wealth is held by the fewest number of people since 1929.”