The View:

The Health and Human Services administration just announced that the average premium for patients on the health insurance exchanges will increase by 25 % in 2017. For those covered in employee insurance plans they are being squeezed between stagnant wages and increasing premiums and high deductibles. The health insurers have a business model that creates profits for them, but creates gaps in coverage (as when a worker is unemployed) with high premiums and high deductibles. Insurers spend billions of dollars on stock buybacks to drive share prices up to increase executive stock compensation. Plus, they spend millions on lobbying Congress to keep their business model in place. These monies could be better spent bringing costs down and reducing premiums. In the final analysis as a country, we don’t need two accounts payable departments – private and Medicare. Let’s move to one single payer system, though it may take years to implement. The Action: Cover the remaining 9 million uninsured with a public option on exchanges, end state by state plans and replace them with a national insurance pool of 360 million, create individual health accounts funded by payroll deductions from salaries for workers and for the uninsured federal basic health and drug insurance would be offered, end COBRA accounts by implementing national health insurance accounts available regardless of employment status, transition employer plans over to health accounts over a 4 year period similar to 401k rollovers into IRA accounts, end penalties for not having health insurance, use the Medicare drug formulary for the industry, end stock buy backs, require full disclosure on health and drug pricing. To implement and guide development of the new health account program we should look at Affordable Care Act exchanges that work like California and those faced with challenges like Oregon. Plus, let’s enlist our progressive investor partners to build new health insurance business models and organizations necessary to make this transition successful.

The Story:

Last week, this author received in the mail a notice from his drug insurer announcing rates for 2017 – a 38 % increase in a standard medication because it was moved to a non-plan brand tier from a generic (it is still generic) and premium increase of 33 %! Recently, my wife made an inquiry about coverage for one her medications where the insurer said her medication was covered was covered but she would have to pay 100 % of the cost because of the tier it was on. What kind of double talks is this? Related to health care, prior to the Affordable Care Act my son couldn’t afford doctor visits because he didn’t have insurance – he would have to pay $150 for a visit instead of a $10 copay. Fortunately, he didn’t have much income so MediCal helped out. It seems that most families or someone you may know has had an issue with a health insurer. Yet, this business model for insurers stays in place. Insurers have designed an inequitable structure to ensure they make money, while those with no insurance or high deductibles are paying exorbitant fees.

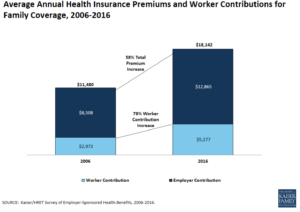

How big is the problem with drug and health insurance? According to the Kaiser Family Foundation insurance costs are going up for those under employer sponsored plans too –29 percent of all workers were enrolled in high deductible plans up from 20 percent in 2014. From 2006 to 2016 workers incurred a 58 % increase in premiums for employer sponsored plans. (click on image to enlarge)

Under the Affordable Care Act (ACA) corporations can move insurance plan costs over to employees for their health insurance and not be penalized. High deductible plans can cause a barrier to care, because patients looking to reduce costs do not go to their doctor or purchase the medicine they need, resulting in more serious illnesses later. This means that while premium costs maybe held in check, high deductibles are dramatically increasing the costs to patients while middle class worker income has stagnated since the mid 1980s. Middle class workers and their families are caught in a wage – health cost squeeze, while drug and health care provider executives make 290 % of an average worker income. The Commonwealth Fund, reports that workers with employer plans spent an average of 6.5 % of their income in 2006 on premium fees and deductibles, this figure soared to 10.5 % by 2015. The squeeze between wages and health care costs is felt most acutely in those states with lower wages. For example, in Florida the average worker spent $16,000 in premiums and deductibles per year, in Massachusetts their health costs were $18,000. Yet, the median income in Florida was $43,401, versus $73,015 in Massachusetts – highlighting the huge squeeze felt in lower income states where wages have not kept up with health costs

Finally, the federal government reports that while another 1 million people will be covered by the public exchanges in 2017 due to the major insurers dropping out, average premiums will be raised by 25 %! For example, Aetna announced that it was dropping 11 states from its plans due to losses of $430M since January 2014. Aetna wants the game played by its rules. Last summer, Aetna told the DOJ that it would bow out of state exchanges if it did not approve their merger with Humana, Aetna also spent $1 billion in stock repurchases in 2014 and approximately $750 million in 2015. Anthem has announced that while it is not repurchasing stock now with its pending merger with Cigna, it still has authorized $4.7 billion dollars! Stock repurchases manipulate the stock price (to drive up price); they do not reduce costs, innovate new services, or compensate employees. In 2014, Humana repurchased $500 million in stock driving the price up by one cent over their earnings target of $7.50 per share entitling CEO Bruce Broussard to a $1.68 million bonus. Middle class workers are caught in squeeze as premiums rise while executives use billions of dollars to increase their compensation that could be used to reduce premium prices.

The success of the public insurance exchanges while contingent on insurer support requires strong state leadership. California supported the public exchange program where 92 % of patients can choose among three or more plans, with increases averaging 15 % for 2017. Most Covered California plan consumers receive premium assistance and qualify for subsidies. Other states like Texas, fought the public exchange plan, and did not accept $10 billion in subsidies over 10 years which left many low income Texans without coverage.

The ACA has been a success with 21 million people gaining coverage, while another 9 million remain uninsured, the lowest number on record. Yet, the pricing and coverage model is wholly inadequate for patients to hold premium costs down and health service providers to manage their businesses effectively while ensuring a high quality of health care.

So how does drug and health insurance work? Drug companies set a price then negotiate an agreement with the health insurer for different tiers of pricing generic (lowest), preferred brand and so forth. The top tier is usually completely uncovered. The insurers negotiate for rebates and discounts to drive patients to certain drugs that the drug manufacturer wants to increase sales, or where they have the highest profits margins. Drug prices increased by 12 % last year, however the insurers saw drug costs increasing by only 2.8%, according to IMS Health. The drug store submits a claim under your plan when you want a prescription filled, the price they submit is high, and not what they receive (it looks big to have the consumer think the insurer is paying the drug store a lot) there are rebates and discount lists, then there is the cost to the consumer as a member. Finally, the plan supposedly pays part of the net amount, but most drug plans make the net figure your out-of-pocket cost. The pricing structure is completely opaque to the patient.

Health provider costs are negotiated as well. On an Explanation of Benefits statement the patient sees the amount the service provider charges, which is not the price the insurer pays which is usually a much lower cost reimbursement. If the patient has no insurance the ‘retail price’ of the service provided is due from the patient. Often these retail costs fall on those patients least able to pay – those with low income or without insurance. Retail costs can be exorbitant for example, an MRI may cost the insurer $1000, while the provider retail cost to the uninsured patient is listed at $10,000. Incredibly, uninsured patients are forced to pay the most for the health services! There is an obvious message here – ‘we don’t care about uninsured patients and we are going to stick prices to them’. For most unemployed patients private plans and private plans on the public exchanges have high premiums, high out-of-pocket or high deductibles. This approach of high premiums, out of pocket and high deductibles don’t work for the consumer!

Insurers have worked hard to keep their business model in place with Congress, Aetna spent over 23 million dollars since 2010 lobbying Congress on legislation that impacted their business, according to the Center for Responsive Politics. Aetna employed 37 lobbyists, with 75 % enjoying a revolving door between government positions and lobbying on behalf of Aetna. The health insurance industry has spent over 61 million dollars in lobbying efforts between 2010 and 2016. These insurer lobbyists are not representing patients.

When the health insurers; Aetna, Cigna, Humana, Anthem threaten the DOJ with leaving the public exchanges and then leave as they did last month, they are clearly undermining the goals for the ACA. They were upset with DOJ for suing all four firms to stop their planned mergers. We need an attitude shift here, how can they make insurance work for all of us.

We have come a long way with the ACA and concessions by the insurers, but they continue to focus on the healthiest patients, increases in deductibles, increasing profits and maintaining high executive salaries. This is all at the cost of patients – all citizens have a right to good, high quality healthcare throughout their life.

The Action

The core need is to provide low cost effective health insurance for people, so when illness strikes patients receive high quality care and become healthy again. Why do we need multiple insurance payers – private and the federal government? If we were running a corporation we would not have two accounts payable departments? We need to transition to individual health accounts that stay with the patient regardless of employment status beginning at birth. Here are ideas on how this transition could work.

Complete Analysis of ACA – We need to learn from the public exchanges that work – California’s public exchange has been quite successful covering new patients, and keeping costs reasonable for low income patients. Yet, we also need to look at why those exchanges like Oregon are not working well and expensive. Let’s summarize the analysis and publish the results so we can build a consensus around the solution, extending what works and recommendations for changes.

Priority One Cover the 9 Million Uninsured – those not covered by insurance need insurance now, we need to figure out how to cover 100 % of our citizens immediately. Offering a public option on the exchanges for basic health services and drug coverage would be a good start.

End State by State Coverage – state pools not large enough to make insurance work for all. With 360 million people in the US we can make our health insurance pool work to reduce costs. Plus, legislation needs to be passed to reverse the Supreme Court decision to allow states to opt out of subsidies. For example, Texas opted out on $10 billion subsidies leaving many low income families without insurance or very high premiums they cannot afford. Interestingly, a few months ago I talked with a small business office manager in Texas, she complained that ACA was not working (her firm did not offer health insurance), for her hourly staff. Obviously, one reason is that Texas opted out of the subsidy program. Using a national pool would help to spread out the disparities between regions in terms of the rising cost of insurance versus stagnant wage increases.

Create Individual Health Accounts – funding can be setup via a payroll tax, accrued to a personal national health insurance account when working (if they don’t have employer options – to be transitioned later). For individuals or families below the regional poverty level they would pay no health payroll tax. For those individuals who are not contributing to their health account, the federal government would fund a basic health and drug account by progressive taxes on wealthy individuals over $250k and the increase taxes on corporate profits. Corporations can offset the increased tax, by offering lower cost insurance, medigap plans or encouraging their employees to move to the basic national health insurance program.

End COBRA – by setting up health accounts regardless of being employed, there is no need for COBRA plans. Otherwise, for those unemployed to continue coverage often they have to pay soaring COBRA premiums up to 400 % of their employed premium rate. For this author, two major illnesses occurred when I was unemployed, often with the stress of being unemployed is the time we need health insurance. COBRA is another example where health insurers are charging outrageous rates to those who need the insurance badly but can least afford it. For the unemployed they could rely on basic health coverage in their individual health account.

Transition Employer Plans – convert employer plans over 4 years into a national personal health care account. Rollovers can be accomplished in a similar way to 401K to IRA rollovers (without the penalty for early withdrawal). Ending employer programs will cut a layer of administration in benefits departments that more rightly belongs to the individual regardless of employment status.

End Penalties For No Insurance – we want to to tax behavior we don’t want and support or subsidize behavior we do want. All Americans who have Social Security numbers should be able to enroll in a personal health insurance account, if they do not have a employer sponsored program. Parents can apply for a SSN for their child to be covered. A public insurance option should be offered to all those families not in employer sponsored programs. The public option run by Medicare is a basic health insurance program run similar to basic Medicare for seniors with medigap plans to cover the other 80 % of coverage needed.

Use the Medicare Drug Formulary – we don’t need multiple formularies and tiers of drug coverage. Medicare already provides one formulary which should be used as the industry formulary. We need to empower Medicare to negotiate all drug prices and health procedures with providers with provision for regional differences on procedures. A critical medication list can be created by Medicare for life threatening (Epipens) or serious chronic conditions (diabetes) capped at 5% profit for drug manufacturers.

End Stock Buybacks by Insurers – insurers need to end stock manipulation and the waste of stock buybacks. Companies like Aetna have spent billions of dollars on stock buybacks which would go a long way to reducing premiums and costs to patients.

Pricing needs to be transparent – similar to a mortgage disclosure statement. The explanation of benefits and drug claim form needs to be clear about the provider or drug price, any discounts and rebates, the price the insurer is paying, the price the provider is actually requiring, the price the pharmacy is paying and the exact out of pocket cost to the patient, with patient accruals in out of pocket and co pays toward insurance coverage.

Do it Without Waiting – let’s get progressive investors to back drug manufacturers that adhere to drug cost reasonable, critical med list, transparent pricing innovative insurance, publicize get more investors on board. Work with Wall Street to setup an ETF stock to focus on companies adhering to the progressive national health programs demonstrating good returns.

Awareness of What Works – A media campaign with surrogates, leadership in Congress, interest groups like the AMA, and the insurers to bring the American people along on the solution journey and to put pressure on Congress to pass the necessary legislation.

Health insurers would focus on medigap plans, taking risk out of innovative drugs to help speed them to market, vision and integrative medicine, personalized medicine, telemedicine – taking their layer out with reduce costs dramatically. They can be contractors to Medicare for transition to health accts. Or insurers can be contract administrators to Medicare, keeping costs low and utilizing their expertise.

Lets establish a lifetime health insurance program that provides good quality care, and low cost medications for all Americans.

(Editor Note: References for this article appear in the Research section of this site.)